The Changing Softwood Market in China

There are numerous ongoing developments and emerging themes in China that continue to impact market dynamics. The economics and/or competitive advantage of various exporters in the supply chain to China are constantly changing, due to factors such as the Russia/Ukraine conflicts, China’s new inspection of pine logs and lumber from certain countries, ocean freight rates, etc. Meanwhile, Chinese domestic consumption of imported softwood logs and lumber in the last two years has been impacted by issues surrounding zero-COVID policies, a sluggish housing market, rising domestic timber supplies, the development of prefabricated concrete and steel construction, etc

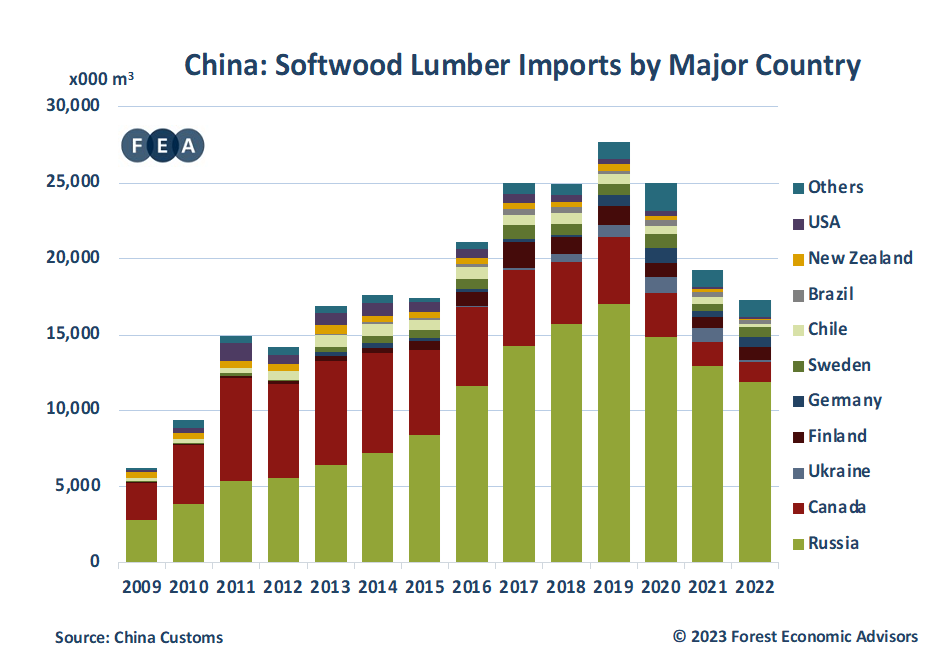

According to statistics released by China Customs, China’s softwood lumber import volume in 2022 was 17.3 million m3, a decline of 10% from 2021. This marks the third consecutive year of decline and is comparable to the import level in 2015. Additionally, China’s softwood lumber imports were nearly 2.7 million m3 in the first two months of 2023, a decline of 3% from the same period of last year.

Of note, China’s new inspection regulation on pine logs and lumber imports, which was implemented in February 2022, has had a significant impact on lumber (particularly for SPF) exports from Canada to China. According to the data released by GTA, Canadian’s SPF lumber export to China in 2022 dropped by 44% to 649,000 m3, representing 49% of total softwood lumber exports from Canada to China. This compares to 61% in 2021 and 71% in 2020. In the meantime, for the same reason, America’s export of Southern Yellow Pine logs to China dropped from 1.96 million m3 in 2021 to only 39,000 m3 in 2022.

China’s emergence from three years of strict “zero-COVID” pandemic in December 2022 delivered a very positive message to the world, and the industry gained much better confidence about consumption demands for imported softwood for 2023. This resulted in a rapid upward trend in CFR prices accepted by Chinese importers for most softwood logs and lumber species in late 2022 and early 2023. However, February and March, a traditionally busy season after the Spring Festival holiday, were very disappointing months for most logs and lumber importers and distributors in China, as China’s consumption demands stayed far below market expectations.

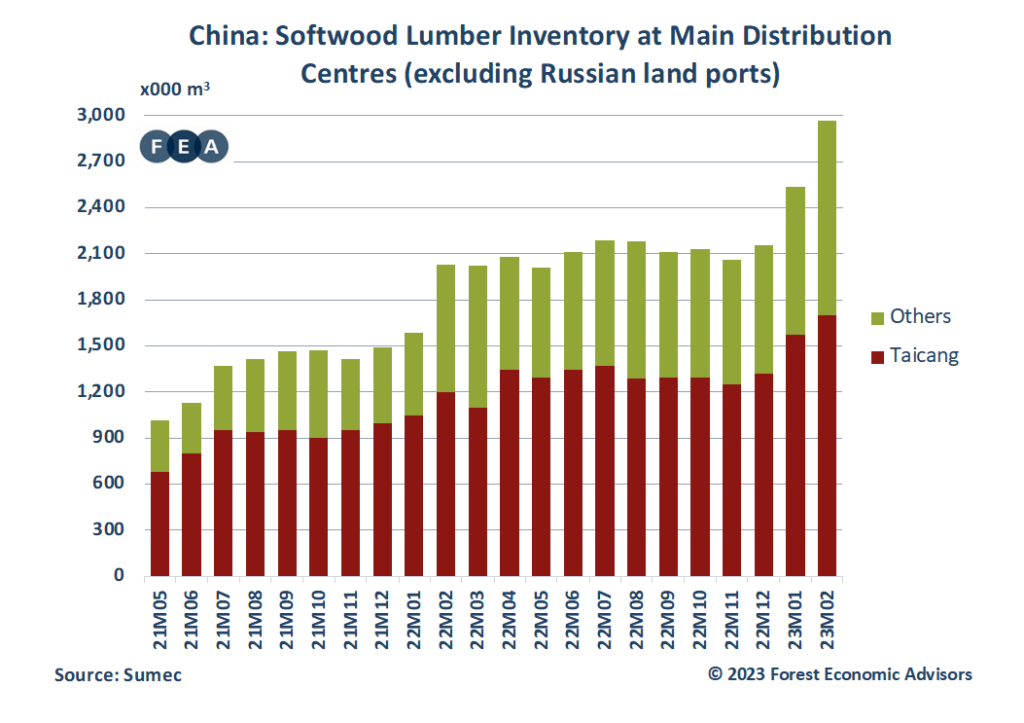

The lumber inventory level at Taicang reached over 1.7 million m3 at the end of February, an almost record high since 2017. Moreover, the high inventory situation occurred not only in Taicang but also in other main distribution centers across China, including Qingdao, Tianjin, Chengdu, Ganzhou and Guangdong. According to the number collected by Sumec, the national softwood lumber inventory at main distribution centers, excluding Russian land ports, reached nearly 3 million m3 at the end of February, a growth of 46% from the same period of last year.

There were two key reasons underlining the rising inventories from the supply side:

- Chinese importers had better expectations regarding market demands in 2023 and took volumes positively from overseas suppliers during 2022Q4 when consumption reductions were seen in Europe and the US.

- Given the dropping volume of Russian lumber imported at land ports, coupled with tough COVID measures at these sites in the last three years, more traders and production mills at Manzhouli and Suifenhe made the choice to move their business to inland areas and ocean ports. This has resulted in higher import volumes and inventories of Russian lumber at those non-Russian-land-ports distribution centers.

- Of all inventories at Taicang, Russian lumber accounts for over 70% of the volume, whereas Canadian SPF’s inventory was 145,000 m3 or 8.5% of the volume.

It’s also worth mentioning that, in addition to the changing imported supplies, the rising supply of domestic timber has significantly impacted the consumption for imported logs and lumber. Although there are no specific statistics showing the exact volume of domestic softwood supplies, however, the market has already felt the rising supply and competition from domestic species, particularly in Southern China regions. It is predicted that the supplies of Chinese domestic species will continue to play more important roles than before in the coming years, given the established supply chain, lower cost, domestic pine beetle epidemic, etc.

There are still no noticeable changes in the underlying fundamentals that would generate higher market demand in various application sectors in the short term. Therefore, what the industry should really worry about is how the country will boost demand – as opposed to focusing on the price/competitiveness of logs and lumber from the various supply sources.