Unveiling China’s Glue-Laminated Timber (GLT) and Cross-Laminated Timber (CLT) Landscape: Insights from an industry wide Survey

In a recent collaborative endeavor between Canada Wood China (CW China) and the China Academy of Building Research (CABR) Certification Center, an insightful market survey on China’s Glue-Laminated Timber (GLT) and Cross-Laminated Timber (CLT) sectors was successfully completed. The comprehensive study encompassed meticulous questionnaires and on-site visits, engaging a cohort of 18 GLT producers and 4 CLT producers. The primary aim of this undertaking was to furnish market players and industry stakeholders with an updated comprehension of the current state and evolvement within China’s GLT and CLT production sphere.

Outlined below are the key findings, and a comprehensive report will be available for download soon.

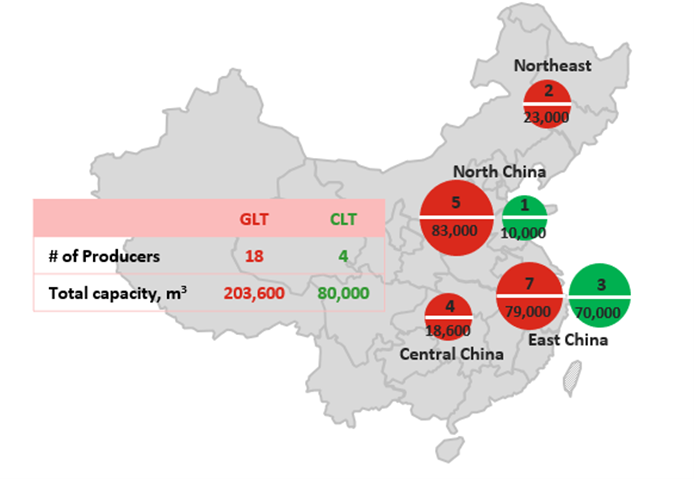

- The research saw the participation of companies that collectively represent over 80% of the market share, encompassing 18 GLT producers and 4 CLT producers. The following diagram depicts the distribution of these essential players within the broader GLT and CLT spectrum.

- All producers exhibit a steadfast focus on the local market and maintain strict adherence to the Chinese production standards. One notable producer conforms to the ANSI standards, underscoring their commitment to robust quality measures.

- Without exception, these producers rely on imported lumber, with 17 out of 18 GLT producers and all CLT producers use graded lumber as their preferred choice.

- The current trend witnessed in China’s mass timber projects leans towards substantial spans and grandiose overhangs. However, the pursuit of standardization and mass production proves arduous under these circumstances. Customization reigns supreme, with the majority of GLT products tailored to bespoke sizes and shapes. Consequently, recovery rates exhibit significant variance, ranging from 50% to over 80%.

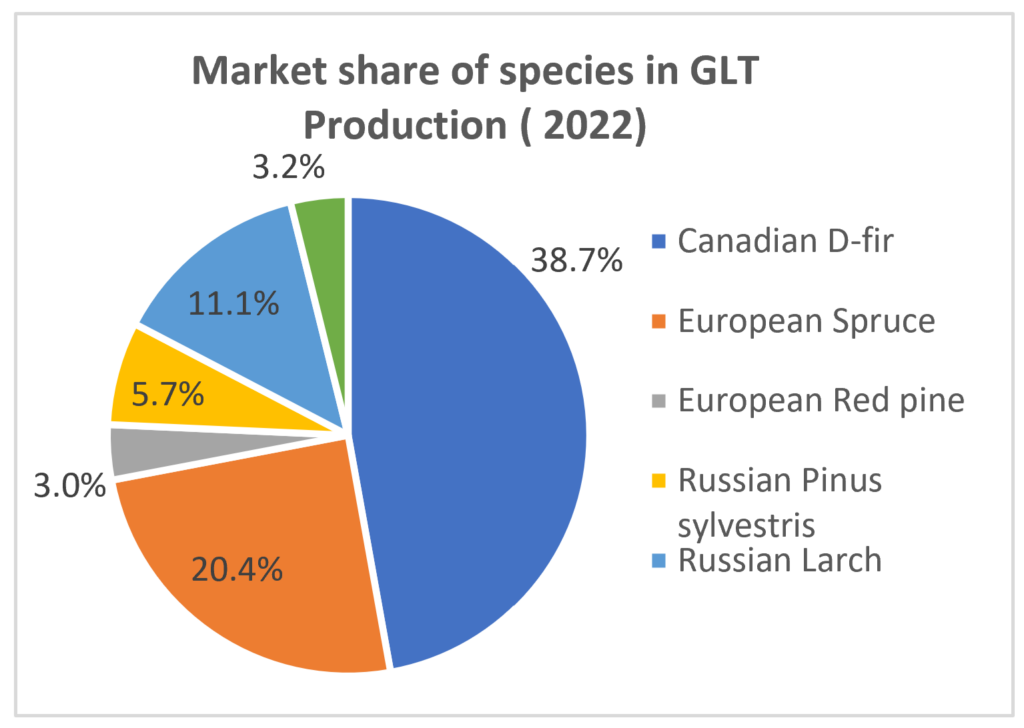

- Unsurprisingly, Canadian Douglas fir reigns the market as the dominant species for GLT production, accounting for a noteworthy 38.7% of 2022’s production. Nonetheless, the utilization of Douglas fir faces constraints due to limited availability and exorbitant pricing, as expressed by the majority of producers.

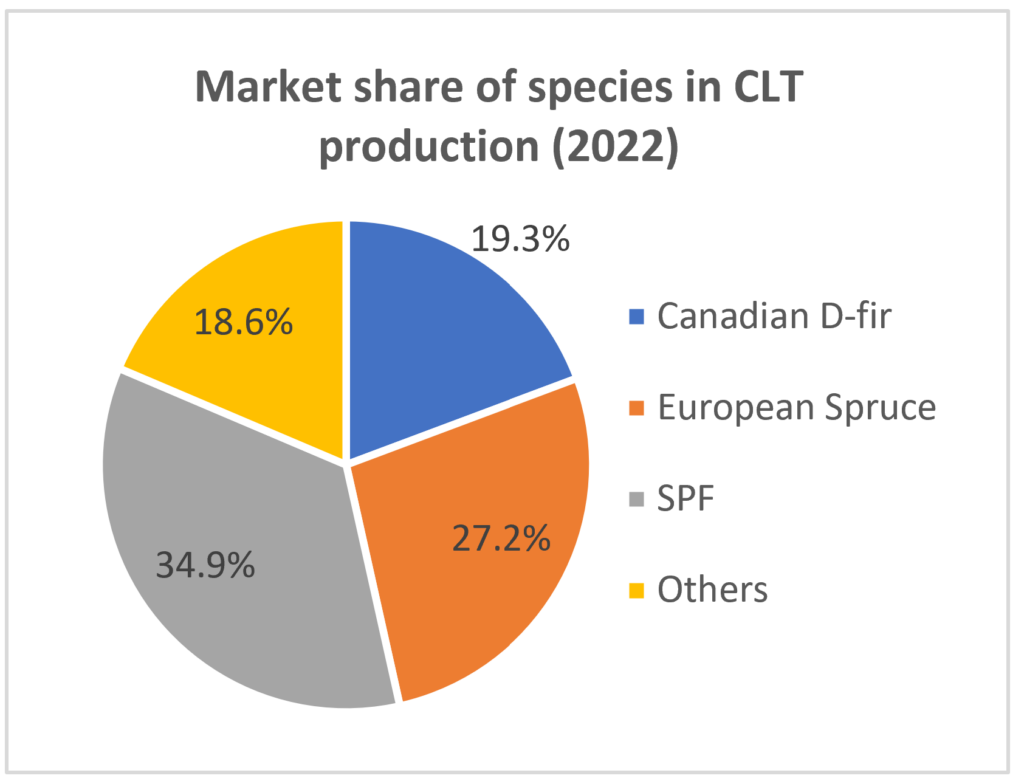

- GLT producers have identified the top three concerns pertaining to lumber usage: foremost being the stability of supply for Canadian lumber, followed by moisture content, and finally, specifications and sizes. European lumber, on the other hand, elicits worries regarding grade, specifications and sizes, as well as moisture content. Concerning Russian lumber, the primary issues revolve around grade, appearance quality, and specifications and sizes.

| No. 1 | No. 2 | No. 3 | |

| Canadian lumber | Stability of supply | Moisture content | Spec & size |

| European lumber | Grade | Spec & size | Moisture content |

| Russian lumber | Grade | Appearance quality | Spec & size |

- The impetus for growth within the GLT and CLT industries stems from China’s dual-carbon strategy and the endeavor to revitalize rural areas. Producers harbor a sense of sanguinity, anticipating market expansion that surpasses overall economic growth. Notably, 14 out of 18 producers envisage an annual market growth rate of at least 10% over the forthcoming 3-5 years, while 15 producers anticipate a self-generated business growth exceeding 10% per annum.

- Acknowledging the indispensability of collaborative efforts in design, engineering, fabrication, and installation, producers exhibit a burgeoning recognition of this vital facet. Employing cutting-edge, high-precision processing machines empowers producers to deliver exacting standards, guaranteeing precise product outcomes and seamless on-site installations.

- Furthermore, producers evince a burgeoning preoccupation with product quality and durability concerning GLT and CLT offerings. Four GLT producers have taken commendable strides by embracing third-party certification (courtesy of CABR with the invaluable support from CW Wood) for their production and products, thus paving the way for enhanced industry benchmarks.